Fast Facts

- Mortgage brokers facilitate over 74% of all residential mortgages in Australia. Mortgage broker commissions are highly regulated under law.*

- Mortgage brokers receive two types of commissions from lenders – upfront commissions, paid when a loan is settled, and trail commissions, paid over the life of a loan.

- The commission rates mortgage brokers receive from lenders is highly standardised across the market.

- Mortgage brokers are required under law to disclose how their commission is structured and percentage to their clients.

- Mortgage broker commission is revenue for a broking business, it is not a broker’s take home pay.

Clients don’t pay mortgage brokers, lenders do

When a broker originates a loan for a lender, the lender pays them a commission – a portion or share of the economic value that the lender expects to earn from the loan.

There are three key components in mortgage broker commission:

Mortgage broker commission is business revenue, not a salary

Out of their commissions, a broker pays for the costs of running their business, including:

- aggregator service fees

- staff salaries and benefits

- regulatory fees (ASIC, AFCA, CSLR etc)

- equipment such as computers and phones

- office rent

- corporate and other taxes

- insurance

- software licenses

- clawback provisions .

Only once all these costs are paid, can a broker pay themselves.

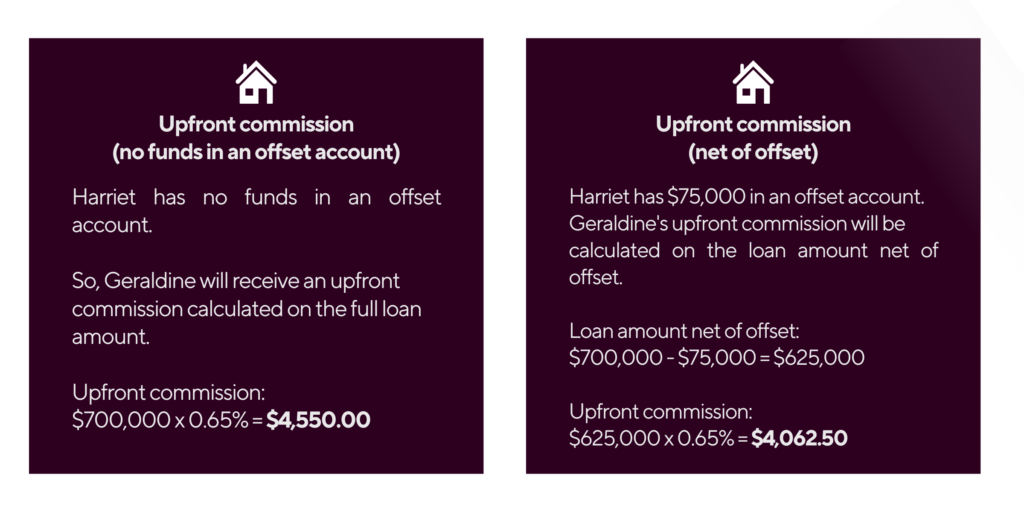

Example

Geraldine is a mortgage broker and facilitates a 30-year $700,000 home loan for her client Harriet. Let’s take a look at the upfront commission (prior to business costs) Geraldine would receive in two scenarios – if Harriet had funds in an offset account and if she didn’t. Based on a 0.65% upfront commission rate (excluding GST).

It’s important to note that mortgage brokers receive commission only after a client settles their loan. It can be up to 90 days post-settlement before a mortgage broker receives their commission.

Choice, competition and consumer protection through the broker channel

Unlike bank staff, mortgage brokers operate under the Best Interests Duty meaning they are required under law to always put their clients’ interests ahead of their own.

Also unlike bank staff, mortgage brokers are able to provide loan options from a range of lenders, and bring choice and competition to the lending market for the benefit of home loan borrowers.